Download the editable 2x2 template here

The AI Value Arbitrage Matrix is a strategic lens for ITES firms under pressure to grow smarter, not just faster.

What it’s good for: Clarifying positioning, aligning resources, challenging legacy assumptions, and structuring growth bets.

What it won’t do: Give you easy answers. This framework surfaces tensions between delivery and economics, perception and pricing, ambition and capability.

If labor arbitrage was your growth engine, what happens when the engine stops pulling?

For decades, the answer to “how do we scale?” was reassuringly operational. You add people. You find efficiency in repetition. You move work to where it costs less to do.

Location shaped your economics. Process shaped your positioning. Margin came from managing the gap between delivery and labor cost.

You didn’t need to own technology. You didn’t need to invent anything new. You needed structure. Predictability. Volume. And that was enough.

But markets shift long before balance sheets show it.

GenAI (while not solely responsible) is an accelerant because it restructures where value resides. It challenges cost-to-serve assumptions and shifts perceived value away from human bandwidth and toward system design.

The wage gap hasn’t closed. But the advantage gap has narrowed in ways that are harder to see yet far more consequential.

That’s what makes this different from previous cycles of optimization.

You’re not just under pressure to be faster or cheaper. You’re under pressure to be structurally smarter.

That’s the backdrop. And in that context, the real strategic question becomes clearer:

If the delivery model is still working, but the economic model underneath it is softening - what exactly are we scaling?

Download the editable 2x2 template here

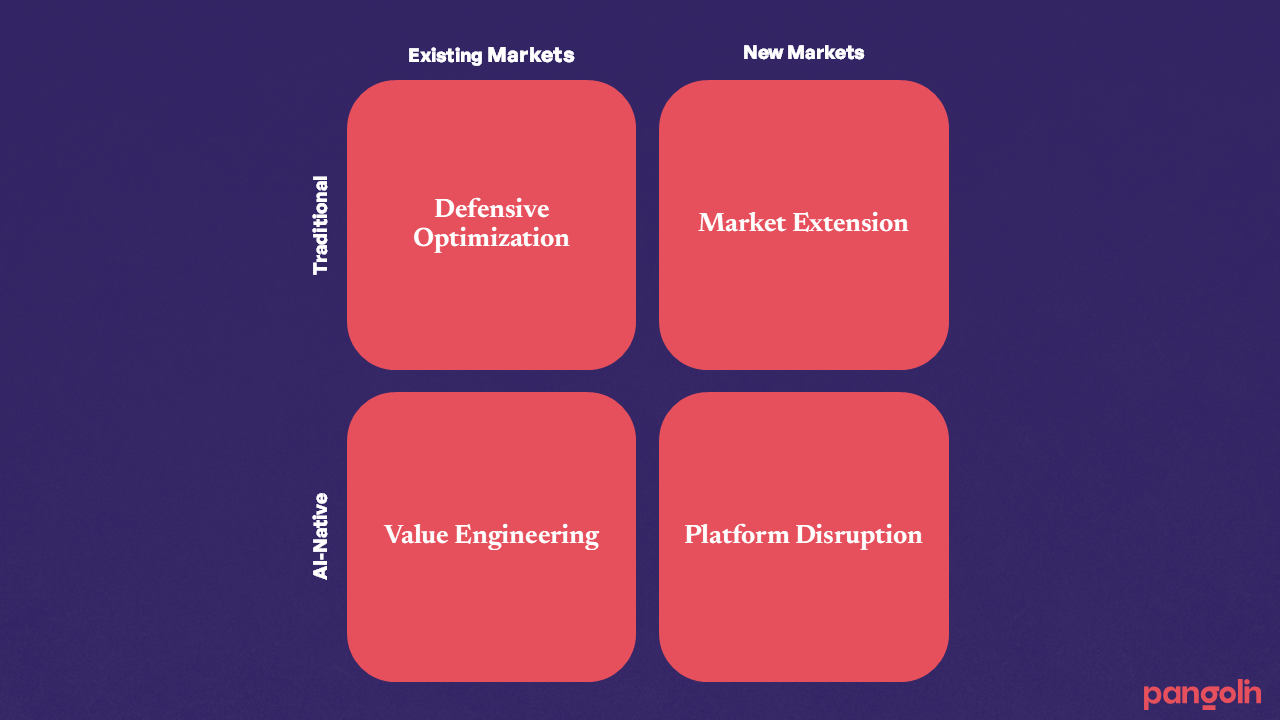

I never did an MBA. But like most people who’ve had to make difficult calls in growing businesses, I’ve come to appreciate a good framework.

Not because it gives answers (Spoiler - It does not) but because it sharpens the questions. This one borrows from Ansoff’s Matrix, except we’re looking at it through the lens of AI disruption in IT services.

You plot two simple variables: What are you selling? Who are you selling to?

That gives you four quadrants. And each one tells a different story about what kind of business you are (or think you are).

Let’s start where most firms are stuck. You take what you already offer, plug in some RPA or LLMs, and hope procurement won’t notice you’ve shaved 30% off delivery time but kept pricing flat.

This is what Infosys and TCS quietly did when they automated 25–30% of back-office tasks. It worked (for a while) as service quality stayed high, average handle times dropped 52%, and clients didn’t complain.

But there’s a catch: 70% of contracts currently are still stuck in time-and-materials. So you gain efficiency, but not leverage. You’re still billing by the hour while AI does most of the work.

This is where things get interesting. Instead of retrofitting AI into old service lines, you rebuild your offer around what the client’s actually trying to achieve: faster contract review, intelligent triage, auto-resolution, you name it.

Example? Infosys again: document processing at 99.5% accuracy, priced at $0.12 per doc not per hour. Suddenly, clients aren’t buying effort. They’re buying outcomes. No surprise that 38% of new contracts are now outcome-based (up from 12% in 2020).

Same skills, different sandbox. Your automation framework built for banks? Repurpose it for clean energy or logistics. Your e-comm ticketing workflow? It probably fits in healthcare too.

This is where a lot of mid-sized ITES firms are heading: reusing the same capability stack, but going vertical or geographic.

It’s not flashy. But it works! Especially when global players are consolidating vendors and expect you to bring “ready-made” to new problems. Yes, CAC goes up. But so does margin - because clients pay for relevance, not origin stories.

Now we’re in venture mode. New services, new business models, new buyer personas. And yes, new headaches.

This is where firms like Accenture and TCS are betting billions on proprietary AI platforms, not just people. They’re chasing 90% automation at sub-$3/transaction cost profiles.

It’s risky. It’s long-horizon. But it’s also where tomorrow’s margins live. By 2025, tech platforms will outpace labor in delivery cost share (60:40)

Most firms don’t realise they’re already investing in one quadrant over others: they’re just not being intentional about it.

What most miss is how mismatched their internal setup is. You can’t hire a bunch of automation engineers and expect them to pitch outcome-based deals. You can’t send delivery folks into AI-native builds and expect innovation. Skills don't stretch across boxes. Neither does pricing logic.

The real question isn’t “can we play in all four?” It’s: where are we pretending we play and what are we really resourced to pull off?

Most leadership teams don’t realise they’ve already made a choice.

You might be hitting all your KPIs today and still be off‐course strategically. You don’t have to inhabit all four quadrants. You need to know exactly which one you’re in and whether your structure, go‐to‐market model, and culture actually equip you to win there.

If any answer feels shaky, that gap is already draining growth.

Download your copy of the matrix here

P.S. We built two simple tools to spark your next move: